Insurance policies can be very confusing. We know how you feel. You look at a policy document. It looks like a foreign language. There are numbers everywhere. One word comes up often. That word is “deductible.” You might ask, what is a deductible? It is a key concept. You must understand it. It affects your wallet directly.

In this guide, we will explain it. We will keep it simple. You will learn how it works. You will see how it changes your premiums. We will look at car, home, and health insurance. By the end, you will be an expert. Let’s dive in together.

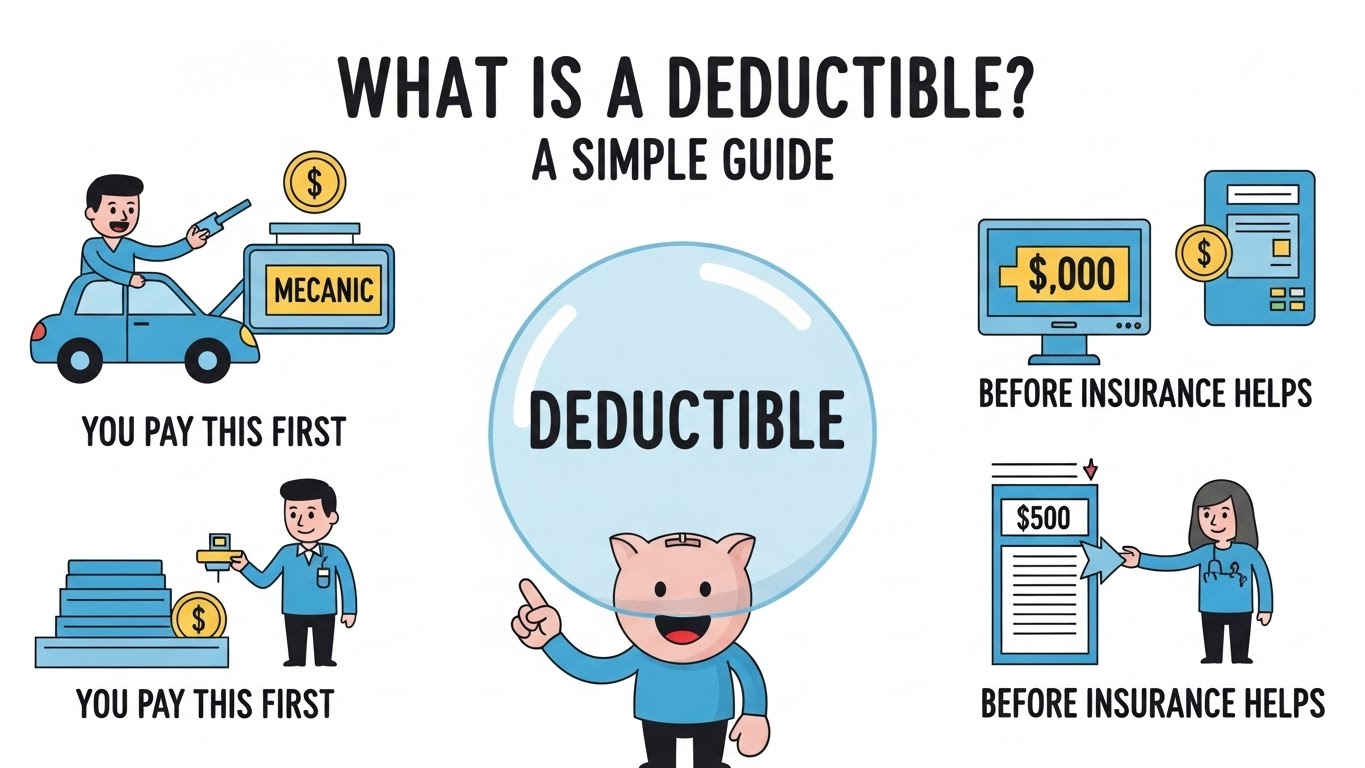

Understanding the Basics

So, what is a deductible? simply put, it is an amount you pay. You pay this before insurance kicks in. Think of it as a threshold. You must cross this line first. Only then does the insurer pay.

Imagine you have a car accident. The repairs cost $5,000. Your policy has a $500 deductible. You pay the mechanic $500. Your insurance company pays the remaining $4,500. You share the risk. It stops small claims. It keeps insurance prices lower for everyone.

Why Do Deductibles Exist?

Insurance companies are businesses. They need to manage risk. If they paid every dollar, they would fail. Processing claims costs money.

If you claimed a $20 scratch, it would be wasteful. The paperwork costs more than the scratch. Deductibles stop these tiny claims. They make you a partner in your protection. When you have skin in the game, you are careful. You drive safer. You maintain your home better.

“The deductible is your share of the financial risk. It is the promise you make to pay your part first.”

The Relationship Between Premiums and Deductibles

This is the most important rule. You need to remember this. It affects your monthly budget.

There is a balance. It works like a seesaw.

- High Deductible = Low Premium

- Low Deductible = High Premium

If you take more risk, you pay less monthly. If you want the insurer to take the risk, you pay more. It is a trade-off. You must choose what fits your life.

Visualizing the Cost Balance

We have created a simple chart. This grid helps you visualize the relationship.

Chart: The Premium Teeter-Totter

| Scenario | Your Deductible | Your Monthly Premium | Who Takes the Risk? |

|---|---|---|---|

| Plan A | $2,500 (High) | $80 (Low) | You take more risk. |

| Plan B | $1,000 (Medium) | $150 (Medium) | Balanced risk. |

| Plan C | $250 (Low) | $250 (High) | Insurer takes risk. |

Note: These figures are examples. Your actual rates will vary.

Deductibles in Health Insurance

Health insurance is complex. It has many moving parts. The deductible here works differently. It usually resets every year. It is not “per incident.” It is “per year.”

You go to the doctor in January. You pay the full bill. You go again in March. You pay again. You do this until you hit your number. Once you hit the deductible, insurance helps.

Coinsurance and Copays

This is where people get stuck. A deductible is not a copay.

- Copay: A flat fee (e.g., $20) for a visit.

- Coinsurance: A percentage you pay after the deductible.

After you pay your deductible, you might still pay coinsurance. Usually, the insurance pays 80%. You pay 20%. You do this until you hit a “max.” This is your “Out-of-Pocket Maximum.” Once you hit that, you pay $0.

Individual vs. Family Deductibles

Do you have a family plan? It gets slightly trickier.

- Individual Deductible: One person meets their limit. Insurance covers them.

- Family Deductible: The whole family contributes. Once the total hits the limit, everyone is covered.

Check your policy carefully. Some plans have both.

Car Insurance Deductibles

Car insurance is different. The deductible is “per incident.”

You crash in February. You pay the deductible. You crash again in November. You pay it again. It does not disappear.

Comprehensive vs. Collision

You usually have two separate deductibles here.

- Collision: For when you hit a car or object.

- Comprehensive: For theft, fire, or weather.

You can set them at different amounts. Many people keep collision high. They keep comprehensive low. Glass damage often falls under comprehensive. Sometimes glass claims have no deductible.

Here is a helpful resource on auto insurance basics from the Insurance Information Institute.

Homeowners Insurance Deductibles

Your home is likely your biggest asset. Protecting it is vital. Home policies have unique rules.

Standard Dollar Amount

This is easy to understand. You have a $1,000 deductible. A pipe bursts. Damage is $10,000. You pay $1,000. Insurer pays $9,000.

Percentage-Based Deductibles

This is common in disaster areas. Do you live near the coast? You might have a hurricane deductible. This is not a flat dollar amount. It is a percentage of your home’s value.

Example:

- House Value: $300,000

- Hurricane Deductible: 2%

- You Pay: $6,000

You must check your policy declarations page. Look for “Windstorm” or “Hail” clauses.

How to Choose the Right Amount

We get this question a lot. “Which deductible should I pick?” There is no single right answer. It depends on your savings.

The Emergency Fund Test

Ask yourself one question.

“Do I have $1,000 in the bank right now?”

If the answer is “No,” choose a low deductible. You cannot afford a high surprise bill. You are better off paying a higher premium. It is safer for you.

If the answer is “Yes,” consider a high deductible. You can afford the risk. You will save money month to month. Over two years, the savings add up.

Grid Feature: Risk Assessment Checklist

Use this grid to decide. Check the boxes that apply to you.

- I have a healthy emergency savings fund.

- I rarely visit the doctor or have accidents.

- I can handle a $1,000 bill unexpectedly.

- I prefer lower monthly fixed costs.

Result: If you checked most boxes, go for a High Deductible.

The High-Deductible Health Plan (HDHP)

You will hear this term often. An HDHP is a specific type of health plan. It has a very high deductible. But it has a secret weapon.

The Health Savings Account (HSA)

If you have an HDHP, you can open an HSA. This is a tax-free savings account.

- Money goes in tax-free.

- Money grows tax-free.

- Money comes out tax-free for medical costs.

It is a powerful tool. It lowers your taxable income. You can save for future health needs. For 2024, the IRS sets specific limits. You can check current limits on Healthcare.gov.

When Do You NOT Pay a Deductible?

Good news! You don’t always pay. There are exceptions.

Liability Claims

If you hit someone else’s car, you don’t pay. Your liability insurance pays for their damage. There is no deductible for liability claims.

Preventive Care

Under current laws, preventive care is free. Annual check-ups are covered. Immunizations are covered. Screenings are covered. You pay $0. The deductible does not apply here.

Subrogation

Imagine the accident was not your fault. The other driver hit you. You might pay your deductible initially to fix your car fast. Your insurance company will then fight the other driver. If they win, they get your money back. This is called subrogation. You get a refund check.

Calculating Your Real Cost

Let’s do some math. We want you to see the full picture. Do not just look at the premium. Look at the “Total Cost of Risk.”

Formula:

(Monthly Premium x 12) + Deductible = Max Potential Cost

Comparison Table: The Real Cost Breakdown

| Feature | Plan X (Low Ded) | Plan Y (High Ded) |

|---|---|---|

| Monthly Cost | $400 | $200 |

| Annual Cost | $4,800 | $2,400 |

| Deductible | $500 | $5,000 |

| Total Risk | $5,300 | $7,400 |

Analysis:

If you are healthy, Plan Y saves you $2,400 a year. If you get very sick, Plan X saves you money. You are betting on your health.

Common Myths About Deductibles

There is a lot of bad advice out there. We want to clear it up.

Myth 1: “I only pay it once for everything.”

Fact: Only for health insurance. Auto and home are per claim.

Myth 2: “My insurance rates go up if I ask about my deductible.”

Fact: Asking questions is fine. Filing claims raises rates.

Myth 3: “I can negotiate my deductible after an accident.”

Fact: No. You agreed to the contract. You must pay the amount set in the policy.

Tips for Managing Your Deductible

We want you to be prepared. Here are smart financial moves.

- Separate Savings: Keep your deductible amount in a separate account. Do not touch it.

- Review Annually: Your life changes. Your policy should too. Maybe you have more savings now. Raise your deductible.

- Bundle Policies: Combine home and auto. You might get a “single deductible” benefit. If a storm hits both, you pay once.

“Insurance is not about making money. It is about not losing everything you have.”

Deductibles and Taxes

We briefly mentioned HSAs. Let’s look deeper.

Medical expenses can be tax-deductible. But only if they exceed a percentage of your income. Paying a high deductible might help you reach this. However, using an HSA is usually better.

For specific tax rules regarding medical expenses, always refer to the IRS Official Website.

Navigating Windshield Claims

This is a unique area. A rock hits your glass. Crack! It spreads.

Repairing a chip is cheap. Replacing a windshield is expensive. Many insurers waive the deductible for chip repairs. They want you to fix it fast. If you wait, the crack grows. Then you need a replacement. That will cost you your deductible.

Our Advice: Fix chips immediately. It saves you money.

The Psychological Factor

Money is emotional. Writing a $1,000 check hurts.

Even if you save money on premiums, the deductible stings. It feels like a loss. This is “loss aversion.”

If you hate sudden large bills, avoid high deductibles. Even if the math says otherwise. Peace of mind has a value too. You need to sleep well at night.

Summary of Key Points

We have covered a lot. Let’s recap.

- What is a deductible? It is the gap you pay before coverage starts.

- It balances with your premium. High deductible means low premium.

- Health insurance deductibles are annual.

- Car and home deductibles are per incident.

- Always keep an emergency fund ready.

Final Thoughts

You are now informed. You understand the mechanics. You can read your policy with confidence.

Next time you renew your insurance, look at the numbers. Do the math. Check your savings. Make the choice that fits your life. Insurance is a tool. You are the master of that tool.

We hope this guide helped you. Financial literacy is a journey. You just took a big step. Stay covered. Stay safe. Save money.

FAQs

1. What is a deductible in simple words?

It is the amount of money you must pay for repairs or medical bills before your insurance company pays the rest.

2. Do I pay my deductible every month?

No. You only pay the deductible when you have a claim or receive medical care. You pay premiums monthly.

3. Is a $500 or $1,000 deductible better?

If you have savings, $1,000 is better to lower monthly rates. If you have no savings, $500 is safer.

4. Does health insurance deductible reset?

Yes. Health insurance deductibles typically reset to zero every year, usually on January 1st.

5. Can I change my deductible later?

Yes. You can usually call your agent and change your deductible at any time, but it changes your premium.